With a year of pandemic restrictions now elapsed, mobility providers in Europe are taking stock of how rolling curfews, travel restrictions and lockdowns have impacted their businesses. Shared mobility operators are no different. But while the sector has indeed been affected by the economy-wide downturn, a new report reveals an industry that has proven remarkably resilient.

At fluctuo, we have just released the first edition of the European Shared Mobility Index, a new quarterly snapshot of the shared mobility industry. This Index benchmarks the industry’s performance for Q1 2021 across shared bike, scooter, moped and car services. Fluctuo selected 16 cities that best reflect the diversity of Europe’s shared mobility markets, analysing aggregated data to offer an overview of recent activity.

Download the Index here!

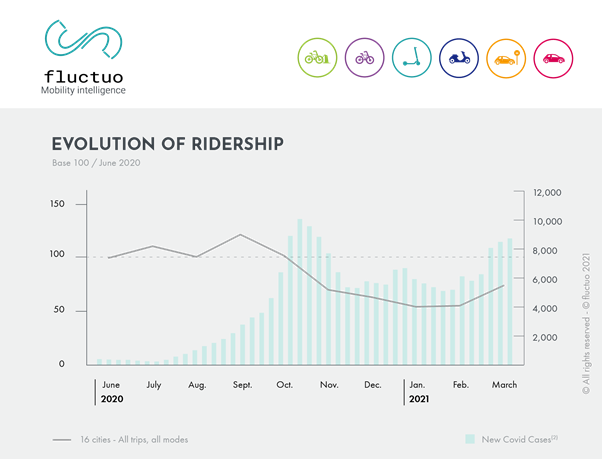

The Index finds that the marked declines in ridership seen across Europe during the first lockdown in March 2020 were no burn out during the rest of the year. In fact, as of 31 March 2021 most shared mobility modes were already approaching the ridership levels seen in June 2020, suggesting the industry is already emerging from the pandemic’s third wave.

Throughout the first quarter of the year, service indicators and performance differed strongly across the four mobility modes. Bike sharing, for example, is present in all 16 cities, with docked or station-based bikes significantly outnumbering free-floating bikes in all but three markets. Scooters have grown to account for roughly a quarter of all shared mobility trips, while Barcelona remains the undisputed king of moped sharing.

The car sharing market is less easily characterized. Business models range from traditional car hire agencies experimenting with app-enabled rentals through peer-to-peer services that lack clear fleet numbers and reliable data. In between, we find a series of established operators (often backed up by major auto OEMs) that offer varying levels of flexibility in car sharing. This results in vastly different fleets of station-based and free-floating vehicles (e.g. Berlin and Paris have almost opposing shares) with even more surprising results for average hourly pricing.

Each edition of the European Shared Mobility Index will also take a closer look at four specific shared mobility markets. The latest report explores Paris and its record-breaking shared services, Warsaw’s growing dynamism, Milan’s well-balanced market and Hamburg’s MaaS ambitions.

Among the Index’s other findings:

- There were approximately 235,000 shared vehicles on the road at the end of the first semester

- Five shared mobility trips were made every second during the month of March

- Nordic cities have the highest per capita vehicle saturation

- Paris has more shared bikes on its streets than 10 of the other 16 cities combined

Of course, the first quarter is typically a period of weak demand and growth. Many shared mobility operators use this time to prepare for the busy summer period, adjusting their fleets, consolidating their services and launching in new markets. The European Shared Mobility Index also charts this behind-the-scenes business activity:

- Eight of the biggest financing rounds raised approx. €171 million for European operators

- Partnerships are intensifying between individual service providers and Mobility-as-a-Service aggregators

- Operators are getting serious about regulatory change, forming multiple advocacy groups at national and EU-level

How mobility operators position themselves for the coming season could have far-reaching consequences for the industry more broadly. Already there are signs of growing consolidation among some of the larger players and a developing trend towards multimodal diversification: some operators now offer bike-, scooter- and moped-sharing all under the one brand.

What is clear from the European Shared Mobility Index is that this industry is redefining urban mobility. Fluctuo is keeping their hands on the pulse with innovative data collection methods, sophisticated algorithms and a team of mobility experts; and it will release the Quarter 2 edition of the European Shared Mobility Index in mid-July. In the meantime, you can access all the findings from the current edition here to learn how the shared mobility industry is emerging from a year like no other